Quick Answer: On expiry day, options premium collapse rapidly (theta decay) and gamma risk explodes in the final hour. Profitable strategies include selling OTM options (if trend is clear), iron condors (range-bound markets), and straddle/strangle selling. WARNING: Nifty weekly options now expire on Tuesday (changed from Thursday — SEBI rule effective 1 Sep 2025). Never hold undefined-risk short options into expiry without a hedge.

Published March 5, 2026 · Last refreshed April 27, 2026. Prices and data are compiled with reasonable care but — always confirm against your broker before trading.

NSE: BANKNIFTY) last Thu / gamma+theta stats.” class=”wp-image-13962″/>

NSE: BANKNIFTY) last Thu / gamma+theta stats.” class=”wp-image-13962″/>Introduction

When Tuesday 3:30 PM IST approaches on NSE, something magical—and terrifying—happens to options traders’ portfolios. The final hour before weekly options expiry becomes a battlefield where fortunes are made and lost in minutes.

You’ve already learned the basics of calls and puts. You understand that options have an expiration date. But here’s what most beginner traders miss: the last trading day of an options contract is nothing like a normal trading day. Option premiums collapse, Greeks swing wildly, and risk explodes exponentially.

This article teaches you exactly what happens on expiry day—and more importantly, how to profit from it without getting decimated by gamma and pin risk.

Key Takeaways

- Theta decay accelerates on expiry day — ATM options lose 50-70% of remaining value in the final 2 hours

- Gamma risk explodes near expiry: small price moves create massive delta swings, especially for ATM strikes

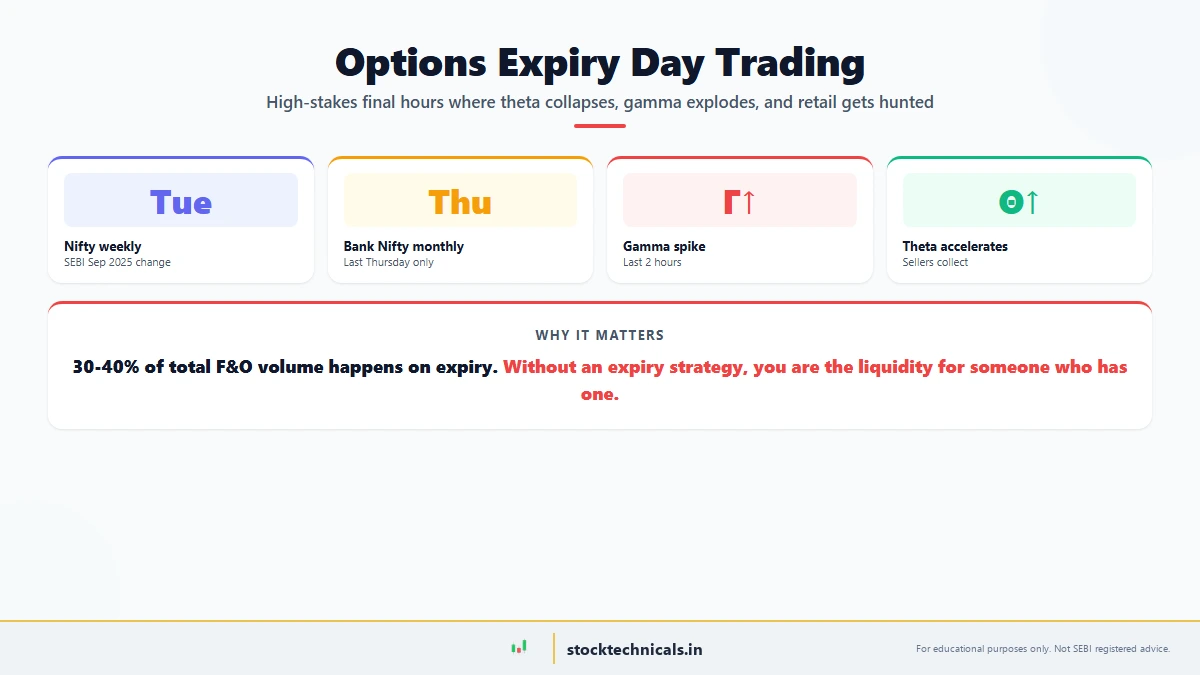

- NSE Nifty weekly expiry is now Tuesday (changed from Thursday on 1 Sep 2025 by SEBI directive)

- Selling OTM options on expiry day works in trending markets; iron condors work in range-bound markets

- Pin risk occurs when underlying closes at or near a strike — settlement can go either way with devastating results

- Use 50% reduced position sizing on expiry day — margin requirements spike and intraday swings are extreme

Why This Matters: Expiry day trading represents 30-40% of total options volume on NSE every Tuesday and last Tuesday of the month. If you’re trading options without a dedicated expiry strategy, you’re essentially playing blind. You’re competing against professionals who have algorithms designed specifically to hunt retail traders on expiry day. Learning to navigate expiry day transforms you from a victim into a participant.

Who is this article for? Traders who already understand option Greeks (delta, gamma, theta) and want to build profitable expiry day strategies. If you haven’t read our guide on options Greeks, read that first—this article builds directly on that foundation.

What Really Happens on Options Expiry Day

Options expiry isn’t just another day. It’s when physics changes.

The Core Concept: On expiry day (typically Tuesday for weekly options, last Tuesday for monthly options on NSE), all options contracts either get exercised or expire worthless. This creates a unique market environment where:

- Theta collapse accelerates — Remaining time to expiry becomes hours instead of days, causing time decay to spike dramatically

- Gamma goes explosive — The rate at which your delta changes becomes unpredictable and violent

- Bid-ask spreads widen — Liquidity dries up as market makers manage expiry risk

- Pin risk emerges — If a stock expires exactly at a strike price, settlement becomes uncertain

The Golden Rule of Expiry Day: “Don’t trade what you don’t understand. Expiry day volatility kills unprepared traders faster than any crash.”

Weekly vs Monthly Expiry: NSE Dynamics

Let’s be clear about what happens every week on NSE.

Weekly Options on NSE:

Every Tuesday, NSE’s Nifty 50 (NSE: NIFTY) weekly options expire at 3:30 PM. Bank Nifty weekly expiry was discontinued in November 2024 — only monthly contracts remain (Bank Nifty monthly still expires last Thursday; Nifty monthly moved to last Tuesday). These contracts trade for exactly 5 days (Monday-Friday of that week).

What’s unique: Weekly options decay much faster than monthly options. By Wednesday (day 4), you’re already losing ₹2-5 per contract per point of time decay on out-of-money (OTM) strikes. By Tuesday morning, premium on OTM options might shrink by 50% within 2 hours.

Monthly Options on NSE:

These expire on the last Tuesday of every month. They have more time decay spread across 4 weeks, which means:

- Slower theta bleed early in the month

- Explosive decay in final 3-5 days

- Larger premium moves (both gains and losses)

- More gamma impact on directional traders

Example: On February 27, 2026 (last Tuesday, monthly expiry):

- Nifty 50 Feb 27,500 CE trading at ₹85 at 8:15 AM

- Nifty settling at 27,540 at 3:30 PM

- That call went from ₹85 to ₹40 in-the-money expiry settlement = ₹27,500 intrinsic value

- Theta decay on that single contract ate ₹15-20 in the last hour

What This Tells You:

- Weekly options are scalper’s heaven—fast decay, quick profit windows

- Monthly options offer more time but extreme endgame volatility

- Most profitable trades happen Tuesday-Tuesday of expiry week

- Sunday expiry (if trading global indices) adds weekend risk premium

Trading Rule for Expiry Week:

“In the final 3 days of expiry, theta decay multiplies. What made ₹100/day in week 1 makes ₹500/day by day 4. Position size accordingly, or get blown up.”

Popular Expiry Day Strategies (And Why Each Works)

Here’s what institutional traders actually do on expiry day.

Strategy 1: OTM Option Selling (The Theta Bleed Play)

This is the simplest and most popular expiry strategy. You sell out-of-money options on expiry day morning, knowing they’ll decay to zero by 3:30 PM.

Example: Nifty trading at 27,450 on Tuesday morning (expiry day).

- You sell 27,200 PE at ₹15 (way OTM)

- You sell 27,700 CE at ₹12 (way OTM)

- By 2:30 PM, both premiums collapse to ₹1-2

- You buy back both, lock in ₹24-25 profit on just ₹27 premium

Breaking down the math: If you trade 2 lots (100 contracts total), your ₹27 credit × 100 = ₹2,700 received upfront. When you buy back at ₹3 (combined), that’s only ₹300, leaving you ₹2,400 profit in 6 hours.

Why it works: Gamma isn’t an issue when you’re far OTM. Theta does 90% of the work. The ₹250 distance from current price to strike acts as a buffer against large intraday moves. Historical data shows Nifty moves average ₹80-120 on regular expiry Thursdays.

Strategy 2: Iron Condor on Expiry Day (The Directional Play)

If you think Nifty will stay in a range (say 27,300-27,600) on expiry day:

- Sell 27,200 PE + Buy 27,100 PE (downside protection)

- Sell 27,700 CE + Buy 27,800 CE (upside protection)

- Net width: ₹100 on both sides = max loss is ₹100 per contract

This caps your profit (all premiums collected) but also caps loss to the width of the short strikes minus premium collected. On 1 lot (50 contracts), if you collect ₹60 premium total and the width is ₹100, your max loss is (₹100 – ₹60) × 50 = ₹2,000.

Step-by-step execution: (1) Sell 27,200 PE at 9:30 AM, (2) Immediately buy 27,100 PE at same market to lock protection, (3) Sell 27,700 CE, (4) Immediately buy 27,800 CE. Complete this sequence in under 2 minutes to avoid price slippage.

Strategy 3: Straddle/Strangle Selling (The Volatility Play)

On high-IV days before expiry, you can sell both a call and put at the same strike (straddle) or different strikes (strangle), betting the index stays inside your strike prices through expiry.

Real Bank Nifty Example (Feb 27, 2026, 1 hour to expiry):

- Sell 48,000 CE at ₹18

- Sell 48,000 PE at ₹16

- Collect ₹34 per contract

- If Bank Nifty stays between 47,966 (lower strike breakeven) and 48,034 (upper breakeven), profit = ₹34 × 50 lots = ₹17,000 on ₹1,00,000 margin

This is riskier than iron condor because losses are technically unlimited if Bank Nifty breaks both sides. However, in final hour with 60 minutes to expiry, Bank Nifty moving beyond ₹100 (2-3 standard deviations) is rare. You’re essentially betting on stable IV and range-bound price action.

Real P&L calculation: If you close this position 30 minutes early at ₹20 total premium (down from ₹34), your profit is (₹34 – ₹20) × 50 = ₹700 per contract = ₹700 on a trade requiring ₹1-2 lakhs margin = 0.35-0.7% return in 30 minutes.

Why it works: You’re collecting both time decay AND betting volatility crashes into expiry. Implied volatility on expiry day morning is typically 20-30% higher than afternoon IV.

Strategy 4: Directional Scalping at Last Hour (The Gamma Trade)

Experienced traders use gamma to their advantage in the final hour. If Nifty is near a support/resistance level and you expect a breakout:

- Buy OTM calls if you expect upside break

- Your delta accelerates as Nifty approaches the strike

- Exit as soon as delta increases (even if stock price hasn’t moved much)

Concrete example: Nifty at 27,400 at 2:30 PM. Strong resistance at 27,450. You buy 27,500 CE at ₹12 (deep OTM). With 60 minutes to expiry, this call has delta of 0.15 (moves ₹0.15 for every ₹1 move in Nifty). When Nifty jumps to 27,430 (only ₹30 move), gamma acceleration makes your call’s delta jump from 0.15 to 0.35. The call is now worth ₹18-20, a 50% gain on a tiny move.

This works because of gamma acceleration—small stock moves create exponential option value changes in the final hour. In normal times, a ₹30 point move might move a deep OTM call by ₹1-2. On expiry day final hour with high gamma, the same move generates ₹4-8 value change.

Gamma Risk: The Hidden Killer on Expiry Day

Here’s what kills most retail traders on expiry day: they underestimate gamma.

What Gamma Does: Gamma measures how fast your delta changes. On expiry day morning, gamma is already elevated. By 2:00 PM, gamma explodes. A normal day’s gamma might be 0.001-0.005. On expiry day final hour, gamma jumps to 0.05-0.20. This 10-50x multiplication means your delta can swing wildly from small price moves.

Why this matters: Imagine you sold an ATM (at-the-money) straddle:

- Sell 27,500 CE (delta = 0.50, gamma = 0.08)

- Sell 27,500 PE (delta = -0.50, gamma = 0.08)

- You think you’re delta-neutral (equal risk both ways)

- Net delta = 0 (neutral)

At 2:00 PM on expiry, Nifty jumps from 27,500 to 27,530 in 5 minutes (₹30 move). Here’s what happens to your deltas:

- Your call’s delta: 0.50 + (0.08 × 30) = 0.50 + 2.4 = overflows to practical 0.85 (you’re suddenly ₹17,500 short calls exposure on 50 contracts)

- Your put’s delta: -0.50 + (0.08 × 30) = -0.50 + 2.4 = practically -0.05 (your puts protection evaporates)

- Your net delta exposure is now 0.80 SHORT Nifty = exposed to ₹40,000 loss if Nifty keeps rising to 27,580

- This happened from a single ₹30 move

You tried to be delta-neutral. But gamma made you massively directional without your permission.

Real Gamma Disaster Examples:

Example 1: March 2024 Nifty Expiry

A trader sold 5 lots of Nifty 22,000 PE expecting Nifty to stay above 22,000. He thought he was safe because:

- Nifty at 22,150 (₹150 above strike = cushion)

- Delta on each PE: -0.15 (minimal downside risk)

- 5 lots = 250 contracts × -0.15 delta = -37.5 delta (equivalent to 37.5 points of downside protection)

At 1:00 PM, RBI announcement hit. Nifty tanked to 21,950 in 10 minutes. Here’s the gamma damage:

- Each PE’s new delta: -0.85 (gamma × 200 point move = -0.15 + 0.08×200 in theory)

- 5 lots = 250 × -0.85 = -212.5 delta = Nifty moved ₹200, but his exposure felt like a ₹1,06,250 position

- He had to buy back at ₹80 premium (from original ₹12 sold), losing ₹68 × 250 = ₹17,000 per lot = ₹85,000 total

- Margin also spiked from ₹1,00,000 to ₹2,50,000, forcing a liquidation

Example 2: Bank Nifty Weekly Expiry, January 2025

A trader sold both 48,000 CE and 48,000 PE (straddle), thinking Bank Nifty would stay at 48,000 ± ₹100. Bank Nifty open: 47,900.

- His short CE had delta +0.35, short PE had delta -0.35 (net delta = 0)

- Combined gamma on both: 0.15 (very high with 4 hours to expiry)

By 1 PM, Bank Nifty rallied to 48,100 (₹200 move). His new deltas:

- CE delta: +0.35 + (0.15 × 200) = overflows to +0.90

- PE delta: -0.35 + (0.15 × 200) = approaches -0.02

- Net delta: +0.88 (short 88 deltas = ₹440,000 worth of short Bank Nifty exposure on ₹5 lakh margin account!)

- He was forced to buy back the CE at ₹95 (profit target lost), and later buy the PE at ₹2.

Breaking Down Gamma Math:

- Normal day: 1-point move in Nifty = delta changes by 0.001-0.002

- Expiry day morning (10 hours left): 1-point move = delta changes by 0.01-0.02

- Expiry day final hour (60 minutes left): 1-point move = delta changes by 0.05-0.20

This exponential relationship is why gamma is called the “hidden killer.”

What This Tells You:

- Gamma spikes 10-50x normal levels in final hour

- Delta-neutral positions become accidentally directional in 5-10 minutes

- Small stock moves become big P&L swings (₹200 move = ₹50,000 P&L swing)

- Hedging costs explode (implied volatility on protective options becomes expensive; protecting a straddle at 2 PM costs 3x what it would at 10 AM)

Trading Rule for Gamma Management:

“On expiry day, reduce position size by 50% compared to regular days. Gamma will punish overconfidence faster than any fundamental event.”

Real Expiry Day Examples: Nifty & Bank Nifty Trades

Let’s move from theory to actual money.

Example 1: Nifty Weekly Expiry (February 20, 2026)

Scenario: Tuesday 9:15 AM expiry morning. Nifty opens at 27,380. Your analysis says it’ll stay between 27,200 and 27,500.

Trade Setup:

- Sell 27,200 PE at ₹28

- Sell 27,500 CE at ₹32

- Collect ₹60 credit per contract

- Trade 1 lot (50 contracts)

- Total credit: ₹3,000

By 3:00 PM, Nifty is at 27,350 (inside your range). Both options are worthless:

- 27,200 PE worth ₹2 (collapse from ₹28)

- 27,500 CE worth ₹1 (collapse from ₹32)

You buy back both for ₹150 total.

Profit: ₹3,000 – ₹150 = ₹2,850 on 1-hour hold (ROI: 95% on ₹3,000 risk if they expire worthless)

Risk: If Nifty closes below 27,200 or above 27,500, losses accelerate. Max loss on this position: width of spread minus credit = (27,500-27,200-60) × 50 = ₹2,200.

Example 2: Bank Nifty Monthly Expiry (February 27, 2026)

Setup: Bank Nifty trading at 48,100 at 2:00 PM (90 minutes to expiry).

You realize IV has crushed and Bank Nifty is unusually stable. High premiums available.

Trade:

- Sell 48,000 PE + Buy 47,900 PE (downside protection)

- Sell 48,200 CE + Buy 48,300 CE (upside protection)

Premiums collected:

- Short 48,000 PE: ₹80 (vs 48,200 CE short at ₹62 = ₹142 total short)

- Long 47,900 PE: -₹45

- Long 48,300 CE: -₹35

- Net credit: ₹142 – ₹45 – ₹35 = ₹62

Trade 2 lots (100 total contracts): ₹62 × 100 = ₹6,200 risk-free if Bank Nifty stays between 47,938-48,262.

By 3:30 PM expiry, Bank Nifty closes at 48,050 (inside your range).

- All 4 legs expire/close worthless or intrinsic

- You keep the ₹6,200 premium

ROI: 6,200 / (100,000 margin used) = 6.2% in 90 minutes.

What These Examples Show:

- Expiry day premium decay is REAL and profitable

- Defensive strategies (spreads, iron condors) limit catastrophic losses

- Final hour trades work best when IV is normal/high (not already crushed)

- ₹2,000-10,000 per trade is realistic for retail traders with proper position sizing

How to Set Up Expiry Trades on Zerodha Kite & Other Platforms

Let’s make this practical.

Zerodha Kite Setup for Iron Condor (Most Popular):

- Open Zerodha Kite, go to Derivatives > Options Chain (or search “Nifty50-27-Mar-26” in search bar)

- Select Nifty 50 > Weekly expiry date (Tuesday of that week)

- Choose your strike spread. Example: Nifty at 27,400, 9:30 AM

– Look for strikes that are far OTM (₹200-300 away)

– Avoid ATM strikes where gamma is highest

– Select 27,200 PE (sell this) + 27,100 PE (buy this) = downside protection

– Select 27,700 CE (sell this) + 27,800 CE (buy this) = upside protection

– Check IV levels: If IV is high (25%+), premiums are fat. Good selling opportunity. If IV is low (15%), premiums are thin. Poor selling opportunity.

- Click Place Order on 27,200 PE:

– Select SELL

– Quantity: 1 lot (50 contracts)

– Order type: REGULAR (not GTT, not AFTER-MARKET)

– Price: Enter ₹28 (slightly below current best bid, increases fill probability)

– Validity: Day (don’t use good-till-cancelled on expiry day)

– Click PLACE ORDER

- Do NOT use “Spread” order type (not user-friendly; causes partial fills). Instead place 4 individual orders:

– Sell 27,200 PE at ₹28

– Buy 27,100 PE at ₹18 (simultaneously, don’t wait)

– Sell 27,700 CE at ₹32

– Buy 27,800 CE at ₹22

– Complete this 4-leg sequence in under 2 minutes to lock prices

- In Positions tab, verify:

– Net short 27,200 PE + short 27,700 CE

– Net long 27,100 PE + long 27,800 CE

– Total credit received: ₹60 per contract = ₹3,000 (1 lot)

– Margin requirement: Shows ₹30,000-40,000

- Set stop loss alerts (in GTT orders section, NOT in orders):

– Alert 1 at 2:00 PM: “Check if profit target ₹30 (50% decay) is hit. If yes, execute 4-leg exit immediately.”

– Alert 2 at 3:00 PM: “Exit 100% regardless of P&L. Market closes in 30 minutes.”

- Set profit target: Exit at ₹30 loss value (50% of ₹60 credit = ₹30 profit locked in). Buy back all 4 legs at market simultaneously.

Platform Comparison for Expiry Day:

- Zerodha Kite: Best all-around. Charts, options chain, Greeks visible, high liquidity. Drawback: UI is complex for beginners.

- Sensibull: Best IV crush visualization. Shows real-time theta decay, how much money you’ll make per minute. Ideal for expiry day trading. Drawback: Requires login to Kite to execute orders (two-app workflow).

- Angel One: Zero brokerage on options (saves ₹60-100 per contract vs Zerodha’s ₹20 brokerage). On a 1-lot iron condor with 4 legs, you save ₹80. Over 10 trades, that’s ₹800. Drawback: Execution speed is slower than Kite.

- Groww: Simple interface, good for beginners. Drawback: Lower options liquidity; you may not get filled at desired prices.

- Dhan: Low margin requirements (saves 20-30% margin vs competitors). On ₹40,000 margin requirement, you save ₹8,000-12,000 per lot. Drawback: Even slower execution; limited Greeks data.

Common Mistakes on Setup:

- Mistake: Forgetting to set stop loss and letting losses run

– Real scenario: You entered iron condor at 10 AM. By 2 PM, Nifty moved ₹100, your P&L is -₹2,000. You think “Let me hold 1 more hour.” By 3 PM, it’s -₹5,000. By 3:30 PM, it’s -₹8,000 (hit max loss).

– How to Avoid: Before clicking SELL, calculate: “If max loss is ₹3,000, I exit at ₹1,000 loss.” Write it on paper. Set a calendar alarm for 2:00 PM: “CHECK IF -1K.” When alarm fires, check P&L. If it’s worse, exit immediately, no negotiation.

- Mistake: Selling too many lots on expiry day (e.g., 10-20 lots)

– Real scenario: You have ₹10 lakhs. You think “10 lots of iron condor = 10 × ₹30,000 margin = ₹3 lakhs. I have room.” But during market hours, if Nifty moves ₹100 against you, gamma spikes margins to ₹5 lakhs. Your broker sends a margin call. You’re forced to liquidate at market loss.

– How to Avoid: Divide your capital by 100. If you have ₹5 lakhs, maximum trade = 5 lots = ₹1,50,000-2,00,000 margin used (30-40% of account). Expiry day margin is already double normal, so position size at half of what you think is safe. Never exceed 40% of account capital in margin on expiry day.

- Mistake: Holding too close to 3:30 PM close and getting surprise gaps

– Real scenario: At 3:15 PM, your spreads are at 90% profit. You think “just 15 minutes, I can get 100%.” At 3:22 PM, RBI surprise news hits. Nifty gaps. Your spreads become losses. At 3:30 PM, forced settlement at market.

– How to Avoid: Exit 100% of position by 3:15 PM on expiry day. No exceptions. Don’t leave anything to chance. Settlement surprises (RBI, Fed, earnings, market halt) happen in last 15 minutes. A guaranteed ₹2,000 profit is better than a potential ₹8,000 loss.

Pin Risk: When Settlement Gets Weird

Here’s something that catches traders by surprise: pin risk.

What Is Pin Risk?

When an option contract expires exactly at its strike price (±1 paisa practically), something strange happens. The exercise rule on NSE says:

- Calls/Puts expire in-the-money (ITM) if underlying ≥ strike at 3:30 PM = automatic assignment

- If it expires exactly at strike = often ambiguous; broker’s system decides

Example: Nifty expires at 27,500.00 exactly. Your 27,500 CE:

- Is it ITM or OTM?

- Will it auto-assign or expire worthless?

- NSE says “options expiring at or very close to strike price may not be exercised”

But “may not” isn’t “will not.” Your broker might exercise it. You suddenly have 1 Nifty futures contract assigned at 27,500, even though you wanted the option to expire worthless.

Real Pin Risk Example:

On June 29, 2023 (Bank Nifty monthly expiry), Bank Nifty closed at exactly 48,010. Dozens of 48,000 PE (strike) holders got surprise assignments, then had to manage futures positions overnight.

How to Avoid Pin Risk:

- Avoid selling options that are exactly ATM on expiry day. Sell strikes that are far OTM (at least ₹100-200 away).

- Exit all positions by 3:15 PM. Don’t let settlement decide for you.

- Check NSE’s official position squaring rules before trading. Rules changed in 2024.

NSE Settlement Rules (2026):

- Options are exercised only if they’re ITM by ₹0.01 or more at 3:30 PM

- Assignments are physical delivery on T+1 (Friday delivery if Tuesday expiry)

- Your broker’s system auto-squashes ITM calls/puts

Risk Management on Expiry Day

Most expiry day disasters happen because traders ignore position sizing.

Rule 1: Halve Your Position Size

- Normal trading: You might use 5 lots comfortably

- Expiry day: Trade 2-3 lots maximum

- Reason: Gamma and margin requirements double. Volatility swings become violent.

Rule 2: Use Spreads, Not Naked Selling

- ❌ Don’t: Sell 10 lots of 27,200 PE naked (unlimited loss if market crashes)

- ✅ Do: Sell 27,200 PE + Buy 27,100 PE (iron condor). Max loss is capped.

Rule 3: Set Profit Target at 50% Decay

- Credit collected: ₹60

- Exit at: ₹30 loss (50% of credit gone to profit)

- Don’t wait for 100% decay. Premium collapses so fast that the last 50% comes with massive gamma risk

Rule 4: Exit Before 3:15 PM Without Exception

- T+1 delivery obligations start after 3:30 PM

- Margin gets frozen

- You can’t exit smoothly

- Rule: 100% out by 3:15 PM on expiry day

Rule 5: Account for SEBI Margin Requirements

SEBI recently changed margin rules for expiry day:

- On expiry day morning, margins are 1.5-2x normal levels

- By afternoon, margins spike further

- Your broker might liquidate positions if you’re undercapitalized

Example: Normal iron condor margin = ₹20,000 per lot. On expiry day = ₹30,000-40,000 per lot.

Pro Tip: Use alerts. Set Kite alerts at:

- 2:00 PM: “Check if profit target hit. Exit if it is.”

- 3:00 PM: “15 minutes to close. Exit all, don’t hold.”

- 3:20 PM: “Last chance. Close anything open.”

Practical Checklist: Your Expiry Day Plan

Before you trade expiry day, run through this:

Pre-Market Setup (Tuesday before expiry):

- ✓ Decide on your strategy (OTM selling? Iron condor? Straddle?)

- ✓ Identify strike prices (where will support/resistance be on expiry day?)

- ✓ Calculate max loss for the spread (= width of strikes – credit collected)

- ✓ Set position size (half of normal)

- ✓ Write down entry prices and exit prices on paper (not in your head)

Tuesday Morning 9:15-10:00 AM (Expiry day):

- ✓ Check overnight news (any RBI/macro surprises?)

- ✓ Look at IV levels (high IV = better premium to sell, but higher risk)

- ✓ Verify your strike prices are still far OTM

- ✓ Place first leg of spread order

- ✓ Execute full spread within 30 seconds (don’t hold partial position)

Tuesday Afternoon 2:00 PM:

- ✓ Check your current P&L

- ✓ If profit target hit: EXIT 100%, don’t be greedy

- ✓ If loss is at 30% of max: EXIT immediately (no averaging down on expiry day)

- ✓ If breakeven: Wait until 3:00 PM for final decay

Tuesday 3:15 PM – 3:30 PM (Endgame):

- ✓ Close ALL remaining positions

- ✓ Accept whatever P&L you have

- ✓ Don’t hold into 3:30 PM close

- ✓ Verify positions are closed on broker statement

Common Expiry Day Mistakes

Mistake 1: Holding ATM Spreads Too Long

The problem: You sell 27,500 CE and 27,500 PE. Nifty is at 27,400. You think “I’m safe, I’m ₹100 away on both sides.”

By 2:30 PM, Nifty is at 27,515. Your 27,500 CE is now ITM (in-the-money) by ₹15. With 60 minutes left, that ITM call has:

- Delta: 0.80-0.90 (massive short call exposure)

- Gamma: 0.15 (will accelerate further with each point move)

- Margin requirement: Jumped from ₹20,000 to ₹40,000

- Your account margin gets frozen. You’re forced to hold, getting crushed by each ₹1 move in Nifty

Real scenario: You have ₹5 lakh account. One iron condor takes ₹80,000 (after doubling on expiry day). If Nifty moves ₹50 against you, your margin calls spike to ₹1.2 lakhs just on margin. Your broker liquidates your entire position at market price.

How to avoid: Sell strikes that are at least ₹200-300 OTM. If Nifty at 27,400, sell 27,100 PE (₹300 cushion) and 27,700 CE (₹300 cushion). If Nifty moves ₹150, you’re still OTM. Only when it moves ₹300+ do you touch strike prices.

Mistake 2: Averaging Down When Wrong

You sold 27,200 PE at ₹28 expecting it to expire worthless. Historical data says Nifty moves average ₹80-120 on expiry days. You’re thinking “I have lots of room.”

But at 2:00 PM, an unexpected RBI statement hits. Nifty crashes from 27,450 to 27,000 in 20 minutes. Your 27,200 PE premium skyrockets from ₹28 to ₹150. Loss: ₹122 × 50 contracts = ₹6,100 on a single lot.

You panic. You think “If I sell 2 more lots of the same PE, I’ll average my loss down. At ₹150, if it comes back to ₹75, I’ll profit.”

Wrong move on three counts:

- You’ve now tripled your exposure from 50 contracts to 150 contracts into the worst scenario

- Even if it recovers to ₹75, you only break even on the 2 new lots, but you’re still ₹6,100 down on the first lot

- By 2:30 PM, if it’s at ₹200, you’re now down ₹100-150 per contract × 150 = ₹15,000-22,500

How to avoid: Cut losses at 30% of max loss. If your max loss is ₹3,000 (iron condor width), exit when loss hits ₹1,000. No exceptions. No averaging on expiry day. Trade rules of legendary pros like Mark Douglas require “Hard stops, no exceptions.”

Mistake 3: Selling Too Close to Strike Price

You’re bullish on Nifty at 27,400. You sell 27,350 PE thinking “it’s only ₹50 OTM, I’m very bullish. Plus the premium is high (₹50).”

Your math: Sell at ₹50, if it falls to ₹25, I profit ₹25 per contract = ₹1,250 per lot. Seems logical.

But by 2:00 PM, Nifty is at 27,330. Your PE is now ITM by ₹20. Premium has jumped to ₹150. You’re suddenly exposed to:

- Margin freeze (your broker might liquidate)

- Gamma acceleration (if Nifty moves ₹30 more, you lose another ₹50-100 per contract)

- Assignment risk (if it expires ITM, you’re short 50 Nifty futures, which means ₹1,36,50,000 notional exposure)

How to avoid: Sell strikes at least ₹100-200 away from current price. “Very OTM” thinking is what pros do; they have risk management infrastructure, multiple positions, and correlation hedging. You don’t.

Mistake 4: Ignoring Margin Pressure

You trade 8 lots of iron condor on expiry day. Normal margin was ₹20,000/lot. You think “8 × 20,000 = 1,60,000 on a 5 lakh account, that’s 32%. I’m safe.”

But NSE’s SPAN margin for expiry day options is 1.5-2x normal. By 10 AM, your margin requirement is ₹20,000 × 1.5 × 8 = ₹2,40,000. You used 48% of your account already.

By 2:00 PM, if Nifty moves against you by ₹100, your margin explodes to ₹4 lakhs due to gamma × deltas. Your account has only ₹2,60,000 left. Your broker auto-liquidates your entire position at market price.

You lose ₹20,000 in forced exit on top of any P&L loss.

How to avoid: Use only 50% of your margin capacity on expiry day. If your account is ₹5 lakhs, trade positions requiring max ₹2.5 lakhs margin (≈ 1.25 lots). Better to miss a trade than blow an account.

Mistake 5: Getting Cute in Final Minutes

At 3:15 PM, your spreads are at 80% profit. You collected ₹60 credit per contract. Your spreads are worth ₹10 now (₹50 profit). You think “let me hold 2 more minutes for that last 20% (₹12 more profit).”

At 3:22 PM, a surprise announcement hits (policy change, earnings, market halt). Nifty gaps. Your spreads turn from ₹500 profit to ₹8,000 loss in seconds. You’re forced to liquidate at market, losing ₹5,000.

Real historical example: September 2023 Nifty expiry, RBI surprise announcement at 3:20 PM caused ₹150 gap in 90 seconds.

How to avoid: Lock in profit at 50-70% of max profit. If your spread can make ₹60, exit when you’ve made ₹30-40. Expiry day’s final 15 minutes are not worth the risk. A ₹2,000 guaranteed profit beats a ₹8,000 potential loss any day.

Comparison Table: Expiry Day Strategies at a Glance

| Strategy | Risk Profile | Capital Required | Best Condition | Typical P&L | Time Commitment |

|---|---|---|---|---|---|

| OTM Selling | Medium (naked) | ₹50K-100K per lot | Low volatility, index stable | ₹2K-5K per trade | 2-4 hours |

| Iron Condor | Low (capped) | ₹20K-40K per lot | Range-bound, unclear direction | ₹1K-3K per trade | 2-4 hours |

| Straddle/Strangle | Medium (capped) | ₹50K-150K per lot | High IV, range-bound | ₹2K-8K per trade | 2-4 hours |

| Directional Scalping | High (delta) | ₹100K-300K per lot | Clear breakout expected | ₹1K-6K per trade | 30-60 min |

| Bull/Bear Call Spread | Medium (capped) | ₹10K-25K per lot | Directional with defined risk | ₹500-2K per trade | 2-4 hours |

The Bottom Line

Expiry day trading is not for beginners. Premium sellers have an edge — but only when they understand gamma, margin requirements, and pin risk. Never hold naked short options into the final hour without a hedge in place. If this article is your first exposure to expiry trading, paper trade for 3 months before using real money. The professionals who win on expiry day have been doing it for years — they’re not guessing.

When does Nifty weekly options expire on NSE in 2026?

NSE: NIFTY weekly options expire every TUESDAY (changed from Thursday effective 1 September 2025 per SEBI circular). If Tuesday is a market holiday, expiry shifts to the previous trading day. Monthly Nifty and Bank Nifty contracts expire on the LAST MONDAY of the month (effective 4 April 2025). Always verify the exact expiry calendar on the NSE website before planning trades — shifts happen.

What is the theta decay pattern on NSE options expiry day?

Time decay accelerates violently on expiry Tuesday. At-the-money options lose 40-60% of their premium in the last 2 hours alone. A 22,000 NSE: NIFTY call at ₹50 at 9:30 AM can collapse to ₹15 by 2:30 PM even if NIFTY is flat. Selling OTM options on expiry day (cash-secured or spread) is a classic income strategy for experienced traders with ₹10L+ margin capacity.

What is max pain theory and how does it work on expiry day?

Max pain is the strike price at which the maximum number of open options contracts expire worthless, inflicting maximum loss on option buyers. Calculate by summing the intrinsic value × OI across all strikes. On NSE: NIFTY Tuesday expiry, price often gravitates toward the max pain strike because option writers (big institutions) profit when price pins near that level. It is not a guarantee — news can override — but a useful reference.

Should beginners trade NIFTY options on expiry day?

No. Expiry day combines all the hardest features of options: violent theta decay, whipsaw price action driven by algos hunting stops, compressed IV with sudden spikes, and premium that can go from ₹50 to ₹5 in minutes. Beginners lose fastest on expiry Tuesdays. Start by PAPER-TRADING expiry for 8-10 weeks, studying how your hypothetical P&L evolves through the final 2 hours. Graduate to 1-lot real trades only after the paper P&L is consistently positive.

What are the top strategies for Nifty expiry day trading?

Four common strategies: (1) Selling far OTM iron condor (sell 300-point-wide spread on both sides, target max pain zone), (2) Short straddle writing 30 minutes before close (collect last-minute premium), (3) Buying cheap OTM options on breakout from morning range (lottery-ticket approach, size small), (4) Calendar spread into next week if IV is elevated. All require Greeks understanding — especially theta and gamma sensitivity.

How does India VIX affect expiry day options?

India VIX measures 30-day implied volatility. When VIX is high (>20), expiry-day option premiums are inflated — better for sellers, worse for buyers. When VIX is low (<12), premiums are compressed — buyers get cheap lottery tickets but lower probability. Track VIX daily: a VIX drop from 18 to 12 in three days before expiry crushes option premium even without a direction move. Plan expiry trades around VIX regime, not just price.

What are the risks of day-trading options on expiry day?

Gap risk — NSE may gap 100+ points at open on news; overnight option holdings can swing ±70%. Liquidity risk — deep OTM strikes have wide bid/ask spreads, getting filled close to fair value is hard. Slippage on exit — in the last 30 minutes, spreads widen 10x. Assignment risk — if you sell options and ITM, you are assigned. Use hard stop-loss orders placed at the broker, not mental stops.

What is the brokerage and tax impact of frequent expiry day trading?

Zerodha charges flat ₹20/trade for F&O; high-frequency expiry trading compounds this — 50 trades × ₹20 = ₹1,000/day. Add STT (0.125% on sell-side premium), exchange charges, GST (18% on brokerage+transaction), stamp duty. Net of all costs, an option sell trade needs ~₹10-15 premium just to break even. Tax-wise, F&O profits are Non-Speculative Business Income; maintain a detailed log for ITR-3 filing and tax audit triggers.

RISK NOTICE

Options trading involves significant risk. Unlike spot stocks, options can expire worthless, resulting in a 100% loss of the premium paid. The SEBI study shows 93% of intraday traders lose money — a disproportionately higher percentage in derivatives. Never risk money you cannot afford to lose. Always use stop losses. Never sell naked options without understanding pin risk, margin requirements, and assignment risk. This content is for educational purposes only and is not investment advice.