Market Pulse · Policy Desk · Published 23 April 2026 · Last refreshed 23 April 2026. Bengal Phase 1 voting today; Phase 2 on 29 April; counting 4 May. Data and price sensitivities described are structural, not point-in-time — always confirm against your broker before trading.

Quick Answer. West Bengal voted in Phase 1 of its 2026 assembly elections today (23 April). Phase 2 on 29 April, counting on 4 May. For traders, the political story is one thing; the market story is narrower: Bengal elections have historically moved a specific set of power sector stocks, but not on the dates most retail traders assume. Across four prior cycles (2006, 2011, 2016, 2021), the biggest tradable moves came 6 to 18 months after the result, not on counting day — driven by WBERC tariff orders, WBSEDCL payment-cycle changes, and renewable auction terms. This article is a structural primer on why. It is not a prediction, not a trade call, not a recommendation.

Who this is for. Traders and investors with existing or planned exposure to Indian power-sector stocks, and anyone wanting to understand the structural linkage between state-level politics and regulated-utility earnings. Intraday traders: most of the content is positional-horizon — election-week volatility is covered in the risk-framing section.

West Bengal went to the polls in Phase 1 of its 2026 assembly elections today. The state elects all 294 members of its Legislative Assembly across two phases — Phase 1 (today, 23 April) and Phase 2 (29 April), with counting on 4 May. Incumbent TMC (Trinamool Congress) faces a more consolidated BJP opposition than in 2021, with Left parties and Congress running a separate front (SDA).

For Indian traders, the political story is one thing. The market story is narrower and more useful: Bengal elections have historically moved a specific set of power sector stocks — but not on the dates most retail traders assume. This article walks through why, what the 20-year record shows, which stocks carry Bengal exposure, and how traders typically approach election windows without confusing political noise with tradable edge.

Key takeaways

- Power is a Concurrent List subject in India — State governments control tariffs, DISCOM health, and renewable policy. That makes state elections structurally relevant to listed power stocks, not just politically relevant.

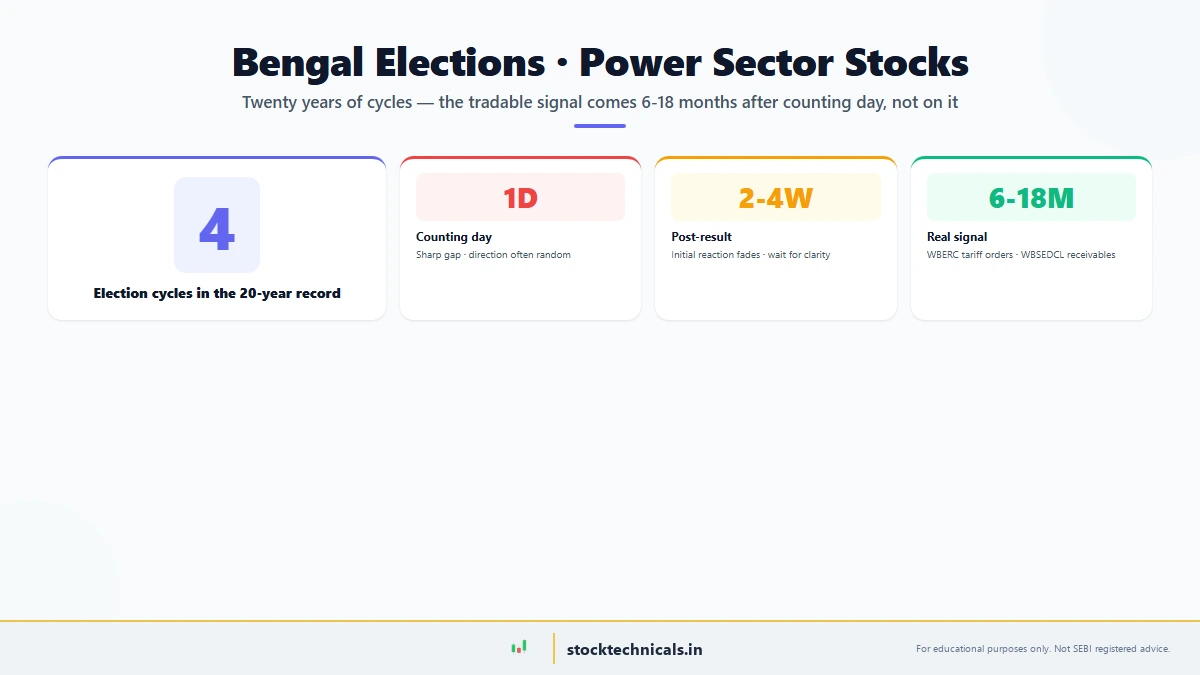

- Across 4 Bengal cycles (2006, 2011, 2016, 2021), the tradable stock moves came 6-18 months AFTER the result, not on counting day.

- Regime-change elections (2011) produce near-term volatility but limited directional impact. Incumbent re-elections produce very little.

- 2026 is different from prior cycles — renewable energy is now bipartisan, the SIR electoral-roll controversy widens the probability distribution, and CESC’s renewable capex plans raise its political exposure vs 2021.

- For most retail traders with no prior view on power-sector fundamentals, trading the election window is speculation dressed up as analysis — best approach is size down, not up.

Why Bengal elections matter for power stocks specifically

Power is a Concurrent List subject in India — both the Centre and States legislate on it. In practice, the State holds the operational levers: tariff setting, distribution licensing, renewable policy, subsidy structure, and the financial health of state DISCOMs (distribution companies) like WBSEDCL. For Bengal specifically, three channels matter.

CESC Limited (RPSG Group’s flagship) is the sole private electricity distributor for 567 sq km of Kolkata and Howrah, serving roughly 3.7 million consumers. Its tariff is set by the West Bengal Electricity Regulatory Commission (WBERC) — a state-appointed body whose orientation can shift with the state government.

State DISCOM health — WBSEDCL serves the rest of Bengal and sells power onward. When its receivables deteriorate, the entire upstream chain (NTPC, Adani Power, Tata Power, independent producers) sees payment risk rise. State government stance on electricity subsidies and cross-subsidies moves this needle.

Renewable project allocations — Bengal is lagging most Indian states on renewable capacity addition. The next government’s renewable policy (auction terms, land availability, off-take guarantees) will directly affect project pipelines at CESC’s subsidiary Purvah Green Power, and national players like ReNew, JSW Energy, and Adani Green.

Election outcomes do not flip these channels overnight. But they reset the 12-24 month policy trajectory — which is where structural moves come from.

The 20-year record across 4 election cycles

Bengal has had four state elections in the 20-year window — 2006, 2011, 2016, 2021. Each offers a different lens.

- 2006 — Left Front returned (235/294 seats): incumbency continuation. Power sector stocks showed little election-specific reaction. CESC traded largely on India power sector beta and coal input cost themes rather than state-specific drivers.

- 2011 — TMC wins, ends 34-year Left rule (184 seats): the regime-change election. Policy uncertainty in the six months around the result produced elevated volatility on CESC. But the stock ended the year roughly in line with sector peers. The real impact came later — changes to Bengal’s industrial policy and land acquisition stance affected new project pipelines over the subsequent 2-3 years.

- 2016 — TMC re-elected (211 seats): incumbency continuation, different mandate. Power stocks traded on national themes (UDAY discom reform, solar auction momentum). Bengal-specific impact was limited.

- 2021 — TMC re-elected (215 seats): held under COVID conditions. Market impact was minimal — the global liquidity cycle dominated everything. CESC’s FY22 performance was driven more by tariff revisions and the start of renewable capex push than by the election outcome.

The pattern that emerges: regime-change elections produce near-term volatility but limited directional impact. Incumbent re-elections produce very little. The bigger moves come 6-18 months after the election, when tariff orders, subsidy policies, and capex approvals begin flowing through — and those moves depend on specific policy choices, not on who won.

EDUCATIONAL CONTENT · NOT A RECOMMENDATION

This article is a historical + structural review of Bengal-election patterns on power sector stocks. Named companies below are examples of sector exposure, not buy/sell recommendations. No price targets. No entry signals. No prediction of election outcome. No characterisation of any political party. If you are a retail trader without a prior fundamental view on power stocks, the takeaway is to size positions smaller around the election window, not to add exposure based on this article.

The stocks in play for 2026

For traders watching this election, the exposure map below covers direct, indirect, and forward-looking categories. Reminder: these are categorisations of Bengal exposure, not trade recommendations. Prices are not quoted — they change daily and are not the useful information in this article.

Direct, high-sensitivity

- CESC Limited (NSE: CESC) — most direct Bengal exposure. Tariff risk, distribution licence continuity, renewable policy all run through state-level decisions.

- RPSG Ventures (NSE: RPSGVENT) — RPSG Group holding company. Indirect exposure to CESC’s fortunes plus diversified businesses.

Indirect, moderate-sensitivity

- NTPC Limited — operates plants including Farakka and Kahalgaon which supply the eastern grid. Policy decisions on payment cycles affect receivables, but the stock is more pan-India than Bengal-specific.

- Power Grid Corporation — transmission utility. Largely insulated from state-level shifts; moves mainly on national transmission buildout capex.

- Tata Power — limited direct Bengal exposure through rooftop solar and EV charging; national-level momentum dominates.

- Adani Power — thermal plant servicing multiple eastern states; Bengal payment flows matter but are not the dominant driver.

Renewable plays (forward-looking)

- JSW Energy, ReNew Power (US-listed), Adani Green, Tata Power Green — all could benefit from a more aggressive Bengal renewable push post-election, though Bengal is far smaller than Rajasthan, Gujarat, Tamil Nadu, Karnataka in renewable capacity share.

What’s different this time (2026)

Four factors separate this election cycle from prior ones:

- Renewable energy is now bipartisan. Unlike 2011, no major party is arguing against renewable capacity addition. This caps downside risk on renewable project pipelines regardless of who wins.

- The SIR controversy. The Special Intensive Revision of electoral rolls has been a central campaign dispute, with voters removed from rolls since October 2025. Whatever the merits, this introduces a wider-than-usual range of plausible outcomes.

- CESC’s renewable transition. Purvah Green Power’s multi-GW target by FY29 is substantial. Tariff economics on these new assets will depend partly on Bengal policy post-election — so CESC is now more politically exposed than it was in 2021.

- Direct TMC–BJP contest. In 2021 the opposition was fragmented; in 2026 the BJP is the clear alternate. This sharpens policy divergence between outcomes and narrows the probability distribution around specific tariff and subsidy paths.

How traders typically approach election windows

The pattern observed across multiple state election cycles:

- Pre-poll window (now through 4 May): volatility builds. Options premiums on Nifty and sector names price in uncertainty. This is not a setup — it is a sizing filter. Reduce position sizes on Bengal-sensitive names.

- Result day (4 May): sharp open-gap move on CESC and allied names. Direction and size depend on whether the result is near consensus (muted move) or surprising (large move). Most retail traders lose money trying to trade the result itself.

- 2-4 weeks post-result: initial reaction usually fades as markets wait for actual policy actions. This is often the best window to re-assess — with clearer information and lower implied volatility.

- 6-18 months post-result: this is where the real fundamental drivers show up. Watch WBERC tariff orders, WBSEDCL receivable trends, new renewable auction terms, and CESC capex commentary. Stocks move on these, not on the election-night reaction.

For most retail traders, the honest truth is: if you do not already hold a view on power-sector fundamentals, trading around the election is speculation dressed up as analysis.

Risk framing

Utility stocks are not meme stocks. Their returns come from regulated tariffs, volume growth, and capex execution — all slow-moving. A one-day election reaction does not change the 5-year return profile of CESC or NTPC.

The one real risk is the tail case — a surprise outcome that triggers a serious policy rethink. This is where stop-losses matter. If you are holding Bengal power exposure into 4 May without a defined exit plan, you are taking binary risk uncompensated. No setup works without a stop-loss.

Bottom line

Bottom line. Bengal voted Phase 1 today. Most of what you will read over the next two weeks about election impact will be noise. The actual tradable signal comes 6-18 months after results, when policy translates into tariff orders and capex approvals. Use this window to build a watchlist, not a trade book. Protect your capital. Everything else follows.

Frequently Asked Questions

When do results come out and when do markets typically react most?

Counting is on 4 May 2026 (Monday). The initial reaction on CESC and RPSG Ventures usually comes on 5 May when markets open. But historically the bigger move comes in the 6-18 months after, when the new government’s power policy actually translates into tariff orders and capex approvals.

Does CESC have operations outside West Bengal that reduce election risk?

Yes — CESC has distribution operations in Greater Noida, Chandigarh, and franchisee arrangements in Kota, Bharatpur, Bikaner, and Malegaon. It also has a thermal plant in Chandrapur, Maharashtra. But Kolkata distribution remains the core earnings driver, and tariff there is set by the state-appointed WBERC. So meaningful Bengal exposure remains.

Should I avoid power sector stocks entirely during the election window?

Not necessarily. The point of this article is not to avoid the sector — it is to right-size positions and recognise that election-week moves are mostly noise. If you were going to hold CESC anyway for its structural renewable capex story, the election is a reason to size down temporarily, not to exit fundamentally.

Which other Indian state elections have historically moved sector stocks similarly?

State-specific sector impact has been visible in: Tamil Nadu elections for wind/solar project pipelines, Maharashtra for highway and construction (MSRDC order flow), UP for sugar and fertiliser (state-controlled policy levers), Rajasthan for renewable auction cadence. The pattern is similar: the election itself produces limited moves; the 6-18 month post-election policy trajectory is where the real fundamental action happens.

Trading in equities, derivatives, currencies, and commodities carries substantial risk of loss and is not suitable for every investor. SEBI’s 2023-24 study showed 93% of individual intraday traders in the equity segment made net losses. This article is educational content only — not investment advice, not a recommendation to buy or sell any security. Political and election references are descriptive of public record; this site takes no political position and makes no prediction of election outcomes. Always paper-trade before risking real capital, size positions so a single loss cannot compromise your financial situation, and confirm every example against your own broker terminal before acting.